Feelings of uncertainty for the global economy and world financial markets filtered through 2016 thanks, in part, to the Brexit vote and US election. The year also saw unexpectedly slow growth in world trade, a pattern which looks set to continue this year.

The most recent World Economic Outlook publication states that between 1985 and 2007, real trade grew, on average, twice as fast as global GDP. In contrast, over the past four years, it has barely kept pace, with few historical precedents for such prolonged slow growth in trade volumes relative to economic activity.

“The empirical analysis conducted by the International Monetary Fund (IMF) in this report suggests that around three-quarters of the decline in trade growth since 2012 can be attributed to weaker global economic growth, and in particular, within that, to the persistent weakness in private business investment,” says economist Saul Eslake. “The remaining one-quarter of the decline was attributable to other factors, in particular, to the dearth of new trade policy initiatives and creeping protectionism, and to an apparent decline in the growth rate of ‘global value chains’.”

Economist Lindsay David says the dramatic slowing of trade growth is a serious issue and worthy of concern, because when trade slows, so too does the global flow of money.

Slow to grow

In 2017, world trade is expected to grow slower than anticipated, according to the latest WTO estimates, with 2016 marking the slowest pace of trade and output growth since 2009’s global financial crisis. “Despite the recent spike in various commodities, in dollar terms weak commodity prices reduce the overall sum of trade, and are deflationary,” says economist Lindsay David. “However, in volume terms, there is enough evidence to suggest that there is more weakness in the global economy, particularly in Asia, than most analysts had earlier predicted. And worryingly, it seems that China may have already, or is very close to, maxing out its domestic demand for international goods and services, and vice versa. Let’s not forget the Trump factor. How he engages trade protectionism will play a critical role in how global trade plays out in the latter half of 2017.”

Lindsay says the dramatic slowing of trade growth is a serious issue and worthy of concern, because when trade slows, so too does the global flow of money. “It can deliver a domino effect as we saw in the GFC and Asian Financial Crisis,” he says. “The big problem now is that we have had for some time excess goods versus demand coming out of China, alongside excess oil stocks, which has put pressure on a lot of countries’ economic performance. This essentially negatively impacts the international flow of money.”

Trump, Brexit and the domino effect

In a year that saw the unexpected election of Donald Trump, Britain’s vote to exit the European Union and challenging domestic economies within numerous nations, there are multiple possible contributors to the unstable trade environment. Interestingly, recent figures also show a weakening in the relationship between trade and GDP growth. While trade has typically grown 1.5 times faster than GDP, in recent years the ratio has slipped towards 1:1.

According to Lindsay, the financial volatility in developed countries has clearly impacted the current global economic climate and resulting trade decline. “We have already witnessed — albeit slowly and for different reasons — what seems to be the early stages of a domino effect whereby a severe economic shift has taken place,” says Lindsay. “Russia, Turkey and Brazil are key examples where, for one reason or another, we saw significant challenges arise within their domestic economies.

“South Africa and developing nations in Asia have seen strong pullbacks on their currencies over the past year and less money flying around their respective economies. Though sometimes the in-the-field experience of feeling what’s happening in a particular economy is not so visible in the official economic data that comes out of their statistical bureaus.”

Brexit panic attack

In 2016, British citizens made the unprecedented collective decision in voting to exit the European Union. The referendum agitated global markets, causing financial panic and continued speculation as to the long-term economic impact of the event. “The immediate aftermath of Brexit was the equivalent of a person walking into a hospital claiming chest pain and the doctors realising it was just an anxiety attack,” says Lindsay. “There was a short-term panic that set in on a market that had a failed Brexit vote 100-per-cent baked in. The adverse happened, the markets fell, and it was a vulture investor’s paradise, picking up the scraps of someone else’s panic over what was a complete over-exaggeration to head for the hills.”

The future impact means the UK will have greater autonomy, believes Lindsay, and aside from financial institutions having to readjust a few elements of their business profile, it will be business as usual. “I can’t see Germany trying to punish the UK through trade barriers or vice versa. There’s no legitimacy in crying over spilt milk when it comes to Brexit.” Saul agrees, and says if anything, the UK economy appears to have strengthened in the months after the Brexit vote. “And of course ‘Brexit’ hasn’t actually happened yet, and won’t for at least another two years,” he says.

“The UK government is still trying to nut out exactly what form it should take. But the most recent British budget announcements suggest that not even the UK government thinks the recent strength in the British economy will be sustained, or that Brexit won’t result in slower growth over the medium term than otherwise.”

Growing anti-globalisation

While trade has declined over the past several years and looks set to continue to follow the same trajectory, anti-globalisation sentiment — though always present — has seen a dramatic and vocal increase. “There clearly is a growing anti-globalisation sentiment around the world — and this should be seen as part of a growing groundswell in favour of greater control by national governments over the movement, not just of goods and services, but also capital and especially people, all over the world,” says Saul.  Trans-Pacific Partnership (TPP)

Trans-Pacific Partnership (TPP)

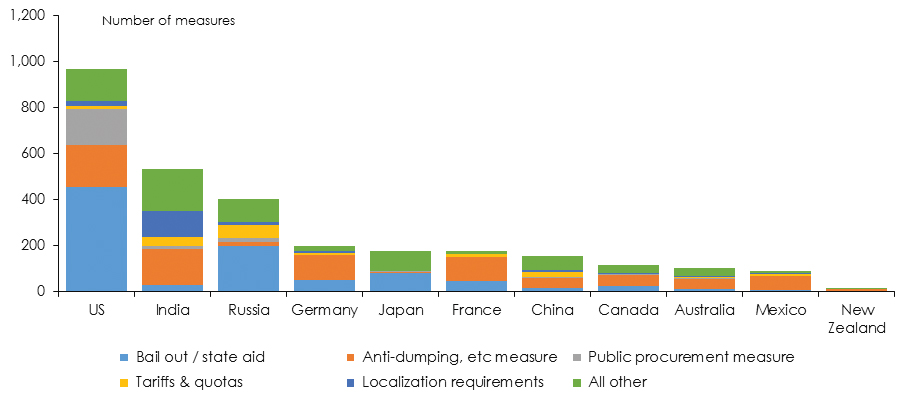

Interestingly, there were elements on both the left and right of the political spectrum that didn’t support the liberalisation of trade and investment. “They were mainly on the left, as evident in the anti-globalisation protests in Seattle in 1999, or in Melbourne when the World Economic Forum had a meeting there in September 2000,” says Saul. “Though also evident in Ross Perot’s and Pat Buchanan’s campaigns in the 1992 US Presidential election.” Fast facts:The US has been the most egregious offender when it comes to implementing protectionist or anti-trade measures since the financial crisis, followed by India and Russia.

However, Saul says that the anti-globalisation sentiment is now more broadly based, unable to be tagged as either left or right. Indeed, such labels are becoming increasingly irrelevant as descriptors of individual political leanings. Fuelled by rising inequality, the anti-globalisation backlash has been further spurred by those who have promoted the ‘freer movement’ of goods and services, capital and people. Another factor is the frustration at the persistent weakness in economic growth since the global financial crisis, and the side effects of that, including stagnant or declining wages and declining full-time employment, especially for people with limited education.

Foreigners are an easy scapegoat

“A good deal of this is more the result of rapid technological change — or of macro-economic policy failures more generally — but foreign goods and services, foreign investors, and especially foreigners, provide an easy scapegoat,” says Saul. “And there’s little doubt that extremists on both the old left and, even more so, the far right have been more than willing to exploit those sentiments to their own ends.”

While the vocalism and increased dominance of anti-globalisation principles looks set to continue, whether these sentiments will be reflected in future trade policy remains uncertain. “This is the trillion-dollar question,” says Lindsay. “Trump seems ready to change the way the world trades with America and where big American corporates manufacture their goods. If the President gets his way, we could expect to see a rhetorical knock-on effect from this. Particularly in a handful of Eurozone nations that follow suit and other nations that may reciprocate any trade barrier slapped against them.”

It’s now critical, says Lindsay, that leaders of large multi-nationals acknowledge the growing trend of social distaste against the corporate world taking away jobs in their home country and sending them abroad. “Finding the right balance between corporate and social responsibility versus profitability will become a growing issue for key corporate decision makers in the years to come.” Naturally, open trade creates both winners and losers.

While the vocalism and increased dominance of anti-globalisation principles looks set to continue, whether these sentiments will be reflected in trade policy remains uncertain.

“As an example, it would be fair to argue that America over the past two decades has lost millions of manufacturing jobs that were transferred to China and other lower cost-of-labour nations in Asia,” says Lindsay. The same can be said for Australia, with much of the manufacturing industry directed to other countries. Though, says Lindsay, Australia did benefit from exporting natural resources.

“The big problem for countries like the US is that it’s hard to be an economy that consumes so much but pays workers in another country to build the products they consume,” says Lindsay. “And particularly in Australia, being a very high cost of labour country, we now have no industry to fall back on aside from mining and housing. These are not exactly twenty-first century industries. At least the Americans have a wealth of next generation industries to fall back on.”

Protectionist policies

As the world’s aversion to globalisation continues to rise, along with economic uncertainty, so too does the possibility that governments will introduce policy to reflect this turbulent climate. “There’s no doubt that there has been a significant increase in protectionist measures since the onset of the global financial crisis,” says Saul. Global Trade Alert lists almost 11,600 protectionist or anti-trade measures announced by governments around the world since 2008, of which more than 9,200 had been implemented. By contrast, over the same period governments had announced only 5,100 pro-trade measures, of which less than 3,300 had actually been implemented. “Interestingly, for all of Donald Trump’s allegations about the US having done badly out of trade deals, the US has been the most egregious offender by far when it comes to implementing protectionist or anti-trade measures since the financial crisis, followed by India and Russia,” says Saul.

The Trump effect on global trade

While Trump has previously indicated his intention to make substantial, sweeping changes to trade policy, global economic factors continue to play a part in the decline of world trade. “Suffice to say there are considerable risks to global trade in the wake of the Trump win in the US,” says economist Stephen Koukoulas. “Even partial implementation of his plans; for a tax on Chinese imports would dislocate trade — it would inevitably be met with retaliation from other countries.” The flow-on effect of such movements would result in far-reaching consequences.

“When trade barriers are built it historically means one of two things — first, the cost of importing goods rise which is inflationary,” says Lindsay. “Second, jobs are commonly lost in the manufacturing country and replaced in the country that puts up the trade barrier. Particularly if the trading partner is the largest economy in the world.” Fast facts:Trade has resulted in Australia’s manufacturing industry being cleaned out and sent to other countries, leaving few industries to fall back on aside from mining and housing.

Indeed, global trade deals aid the improvement of the flow of money at a global scale, with the greatest beneficiaries of free trade undoubtedly large multinational corporates, able

to significantly reduce their cost of manufacturing. Of course, consumers also benefit financially from free trade, though this is offset where quality of goods sold are compromised.

So, what then for the future? “We live in a world that seeks global economic efficiency,” says Lindsay. “This means that to make the global trade system more efficient the world is going to have to focus on how to speed up the time it takes to send goods from one side of the world to the other. Otherwise, we must be very close to exhausting all other channels

of efficiency.”

While much of the future outlook will depend on how Trump rolls out his trade policies, Stephen says the conditions for a turning point in global trade are in place. “Sustained economic expansion in the US and unambiguous signs of stronger growth in the Euro area should underpin a pickup in trade, which will be enhanced by a turning point in Chinese economic activity,” he says. “The recent upswing in commodity prices reflects enhanced trade prospects. The world is close to the low point in the cycle for trade.”